Caroline and Joey have 529s. I can't remember much about how we chose that route, but it seemed the very best one at the time. #notveryhelpful.

I'm interesting in hearing what people think too. We set up Coverdell accounts (aka Education IRAs) which are freely invested accounts equivalent to a Roth IRA (post-tax contribution, all disbursements tax-free) but are more limited in contributions (2k/year/kid.) That should approximately cover the cost of meals by the time our first gets to college.

We haven't done 529 yet just because they seem so restricted and fee-heavy.

Whatever you do, don't stash the money in a VW Beatle. Not very safe at all.

The former college admissions person I know was very cynical about savings marked for college. She felt that most of the middle-class applicants she was seeing got badly burned in the financial aid process -- that in essence their parents got "punished" for saving for their educations.

I don't work in that field and don't have any hard data, so I'm curious to know what better-informed people think. I do believe that in general it's better to have fungible savings than ones that are required to be used for a certain purpose. A person might grow up and want to use the money for Olympic training, or international travel, or even (heaven forbid) medical expenses. Having it locked into a system that requires you to spend it in one relatively narrow category seems unnecessarily limiting.

There's some distinction about who owns which types of accounts in terms of financial aid. Custodial savings accounts in the kid's name are the worst because they offset financial aid at a higher rate than parental assets. I forget where Coverdell and 529 fall- I think it depends who is the beneficiary and who is the owner, although there was some recent change to this that I think made them entirely parental assets.

Based on this site, it looks like the best strategy is to buy a primary residence with all your and your child's assets the year before college, then sell it a year later and buy a new house worth X less where X is the cost of tuition, and repeat every year using the proceeds to pay the college bill. Or give everything you own to the grandparents.

You should do exactly what I've done: have AB take care of it.

Same deal with laundry, incidentally.

Any other questions?

To expand a bit, my understanding is that we have a 529 for each kid. Also, we will have this house paid off by the time Iris goes to college, which is how we expect to be able to have anything available to pay.

We have 529s. They have "worked", but not to any huge benefit.

That said, I would *not* start a 529 right now for her--the treatment of these things has changed every few years. Right now I believe they are treated as a parental asset (or even not at all in some cases! but he article warns this "loophole" might be closed), but before '06 some at least were counted as assets of the student (and student assets do get dinged at a far higher rate). The link is a pretty comprehensive discussion of current practice, emphasis on *current*. I'd stick with something more fungible right now.

6: One question -- what's AB's number?

AB should also be employed to run your film serieses.

She felt that most of the middle-class applicants she was seeing got badly burned in the financial aid process -- that in essence their parents got "punished" for saving for their educations.

I don't work in that field and don't have any hard data, so I'm curious to know what better-informed people think. I do believe that in general it's better to have fungible savings than ones that are required to be used for a certain purpose.

Amen to all of that. My parents weren't middle class at all, and got burned badly, which was pretty incredibly devastating for them, since they really didn't have a lot saved anyway (for me or for themselves).

Just open a savings account and put money into it. Or, for a higher return, buy CDs or government bonds. I wouldn't mess with anything else.

(Note: 529s probably avoid the worst of the ways people get screwed. I don't really know much about them. But my sense is that they're also probably more trouble than they're really worth, in terms of administrative hassle, etc. vs. extra returns.

I'm tempted to just say screw it, one of my in-laws works in the financial industry and will probably get a big enough bonus this year to cover all college expenses.

I recommend marrying into money as the prudent plan.

The system for financing college education in this country is as broken as the system for financing health care.

How much money do you have? Okay, that's how much you have to pay for college. $10,000? $0,000? $50,000? Whatever your savings are, that's the price.

they're also probably more trouble than they're really worth, in terms of administrative hassle, etc. vs. extra returns.

They do save you from paying any capital gains tax on earnings, which adds up when you're talking about tens (or hundreds, at the rate tuition is going up) of thousands of dollars. It's pretty much the same hassle-to-benefits ratio as an IRA.

What happens to 529 money if it doesn't end up being used for college expenses (for whatever reason)? Do you just have to pay all the back-taxes in order to pull it out of the account?

529s have an immediate state tax advantage lots of places, so immediate return at your state's marginal rate of taxation. They're a handy vehicle for gifts, not relevant for my family. Otherwise, yes, fees and bad choice cost 0.3-1% annually. Maybe still a good option because they are so easy, at least up to the state tax exemption limit.

College savings strategy depends on how much wealth+income you expect to have at admission time, as others have said. If you expect aid and lean towards cynicism, hidden gold would be a pretty clear choice. Also, universities deplete parental retirement plans less aggressively than other assets right now. Those (IRA and Roth) can be used as security for loans, so you can still use the money. Also that route gives some parental control if offspring has bad judgement at 18.

I recommend marrying into money as the prudent plan.

Wow, did I fuck that strategy up badly. Plan B is to put crushing pressure on Rory to secure full scholarship support.

What happens to 529 money if it doesn't end up being used for college expenses (for whatever reason)? Do you just have to pay all the back-taxes in order to pull it out of the account?

Plus a 10% penalty unless you qualify for certain exemptions (i.e., death, disability, you got in to the Naval Academy, etc.)

That's only if you withdraw it, though. You can just leave the extra in there and change the beneficiary later without any penalties. Instant college fund for your grandchildren!

10% of the earnings, I should say, not the principal. The penalty isn't quite that confiscatory.

And yes, if you run your financial strategy is to minimize your EFC (Expected Family Contribution) you will not have your children have assets (or nor should you really, spend it all!) and will have as much as possible of what you do have tied up in your primary home (but forgetting even the potential changes over time in rules, the treatment can vary by college--pure FAFSA EFC is a common calculation, but all schools ask for supplementary information and use it and the basic FAFSA info as they see fit).

In some sense I have gotten "burned" (and continue to do so) since we have been quite frugal. Does not bother me in general--I saved for college, now I'm spending for college and my kids are spending some current and future money as well. If things go flub in my financial life in the near future I will certainly find some room for anger or remorse; I *was* a bit chapped to discover that a family we know well had an EFC about 60% of ours (but hey! they had an in-ground pool) even with similar income but it does not keep me up at night. (Unlike the utter week of rage I experience when we gather and fill in all the bullshit forms and supplementary forms etc. The worst is the year when they are applying, especially if you and your kids have bought into the UMC College Death Cult practice of applying to a zillion schools and you need to fill it out for *all* of them. It is better later when it is just the ones they are attending.) It really is a mess, but I cannot say that me or my family are at a disadvantage in the larger scheme of things with regard to higher education other than in comparison to the cheaters who are cheating me, society and the country in multiple other ways.

Aargh! Unfogged is doing nothing to alleviate my late-empire fatalism these last several days.

Aren't plans like this just like the mortgage interest deduction as far as inflating the price of what you're buying? If they provide a government subsidy to save an extra, say, $10k, that just allows the colleges to charge an additional $10k. I think part of the reason college prices are going up so fast is because they've convinced everyone that it's proper to put aside as much as possible for college and mortgage your house to pay for it.

If you expect aid and lean towards cynicism, hidden gold would be a pretty clear choice. Also, universities deplete parental retirement plans less aggressively than other assets right now. Those (IRA and Roth) can be used as security for loans, so you can still use the money. Also that route gives some parental control if offspring has bad judgement at 18.

So a reasonable course of action would be to dump whatever we'd be setting aside for Hawaii into a retirement fund, and then finance Hawaii's education mostly by taking out loans?

I've heard this advice before, actually. It just feels a little scary to count on taking out loans. Is anyone in the process of doing this?

21: Should amend to say assets in retirement funds are better than house.

Lalalalalalalalala I can't hear any of you.

One more comment: what will potentially be a far bigger factor (and one I was not as prepared for as I thought I was) is the differences in undergrad costs. The per year costs for the various school choices for my eldest (after scholarships etc.) were basically 1x, 2x, 3.5x and 5x where x was the cost at the cheapest. This (very fraught) choice represented a much bigger impact to the bottom line than the deltas from any savings or asset strategy.

26: Huh. I had the impression, based on no real knowledge, that once you were getting financial aid at all, that the sticker price evened out -- more expensive school meant more aid. No?

Sure to 23, after keeping 8-12 months living expenses + 1 year tuition in liquid, ideally off-the-books form.

I expect to be in this position (loans secured by retirement funds) after divorce, no idea if I will be funding my kid's education with or without help. Secured loans are a pretty stable institution.

FWIW, I think there's a real chance that education will be much cheaper, in that the premium from having attended strong undergrad schools will diminish very much wrt just learning material wherever and passing relevant tests.

27: For our first we qualified for no financial aid other than loans. This was state school, great scholarship; state school nominal scholarship; private school scholarship; private schools no scholarship. And even if you get financial aid at a "top" private, there will likely be far cheaper options at public schools (though who knows x years from now).

I seem to recall that the worst financial aid package I was offered, back when I applied to college, was at a state school (in a state I was not a resident of). I would be surprised if good public schools really are that much cheaper than comparable private schools. Not that I know a damned thing about college costs, really.

28.last: I'm mixed on this. On the one hand distance learning and test-based credentialism is poised to erode a lot of it. On the other hand, Harvard could probably charge $250K/year on the free market and fill its freshman class with generally qualified candidates

30: would be surprised if good public schools really are that much cheaper than comparable private schools.

For someone getting a lot of financial aid, this is true. If you aren't, there is a very significant difference in cost (particularly for in-state schools in most states).

I'm leaning towards 25 as the best strategy.

We set up 529s for each kid on the advice of our financial guy, and I'm just hoping by the time they're old enough for college the Miracle of Compounding Interest (along with the Miracle of Generous Grandparents) will solve any potential problems.

28.last seems to totally miss the point of why a good school is worth going to, but so do most students, so it may be reasonable.

33: Unfortunately students don't become cynical enough to understand the importance of networking until just after the networking opportunities end.

re: 34

Tragically not true. In my experience, there's a minority who know exactly what they are doing.

re: 28.last: One learns from the other students, of course, but if many of these fail to attend well-ranked universities, and there's a way to find them, kids can still come out aheadin education and have airfare to Madagascar or wherever left over, instead of loans.

For kids that absolutely don't know what to do, the sheltering environment and easy palette of choices may be valuable-- but why not sit out a year working until you DO know that you want either economics or biology in that case?

For kids that absolutely don't know what to do, the sheltering environment and easy palette of choices may be valuable-- but why not sit out a year working until you DO know that you want either economics or biology in that case?

This is probably sensible advice, but I think a lot of parents would fear that their lacksadaisacal little 20-something will never get around to going to college, and then will accumulate a child or two, at which point it will be a much more difficult for them to get that degree, and they'll be locked out of a lot of good-paying jobs.

37: Another possibility is that lackadaisacal kid will play along with parental expectations and go to fancy expensive college, and then decide they don't know what to do and drift from one low-paying job to another continuing to expect parental financial assistance from time to time.

This started out to be about my brother's kids, but then I realized it wasn't too far off from my own career/financial trajectory.

Sure, but the parents of the lackadaisacal kid won't fret about that for four years later than they would have if the kid was redshirting on college a year or two. And that four years can stretch out even longer if the kid fails a lot of classes in college.

When HP goes to college, there won't be public universities -- at least not as we think of them now. That's for you, JP; just humming a few more bars of the late-empire blues.

39: Clearly, you've got this parenting thing all figured out heebie!

assets in retirement funds are better than house.

JP hosted Thanksgiving in his IRA this year.

41: Of course she does; otherwise she wouldn't have become one!

42: Yes. I almost further amended to add, "But you get to live in the house" (or "swin in your pool"). "Better" in 24 is only in the sense of lowering your EFC.

42: Actually, he meant House, the TV series.

25: Wow, LB is finally learning to really appreciate music!

Yeah, that's the flip side-- if the public universities, which are a source of a cheap good education for lots of motivated kids, really do collapse, then saving looks pretty important. On the other hand, that would put a lot of talented kids into community college or distance learning, thus improving the reputation of these channels.

When will the states actually begin dismantling campuses and leasing the land, Ari? Of course, the administration payroll will not be affected by the loss of students or of campuses.

HEY! We gave you that land FOR A REASON, Ari. If you start dismantling the land grant colleges, I'm going to have an opinion about that.

Invest in Franklin CDs. Obviously.

48: Hey, kids! I've got an idea for that land:

A journey. A saga. A legend. The World is today's great development epic. An engineering odessey to create an island paradise of sea, sand and sky, a destination has arrived that allows investors to chart their own course and make the world their own.

There will always be the über-rich; what could go wrong?

I follow the innoculation strategy: send the kid to private school so you can get accustomed enough to writing painful tuition checks that you won't notice when they double or triple. But I don't think it's really going to work.

I am a bit skeptical about most tax-advantaged investment plans. You have to trust the government not to change the rules for longer than I'm really comfortable with, and investment providers are very good at figuring out how to skim 2x in fees off the account you set up to save x in taxes.

This has mostly already been said, but even though it sounds like a joke, the degree to which 13 actually is the honest-to-god, no-bullshit plain truth of the matter can't really be overstated. It's really not at all clear to me that saving in advance for your kids' education is a good idea. (Or at least: saving in any form that's reported/counted in the aid calculations.)

And yet, "Pay what you have" sounds a lot more egalitarian than, "Attend only if you can pay." Vaguely Marxist. Kind of like speeding tickets in Sweden- pay a percent of your worth rather than a flat fee.

53: Egalitarian except for the genuinely wealthy. It comes down to "We'll take all your assets (barring your domicile) up to the full sticker price of a college education." Everyone with less in assets than the full sticker price (which is most people, but not everyone) comes out stripped, everyone with more gets to keep the excess.

Give the money to Reverend Larry. He'll send bibles to El Salvador.

Well, the right way to do it is, "Pay a percent of your worth," with no upper limit, but good luck with that.

And yet, "Pay what you have" sounds a lot more egalitarian than, "Attend only if you can pay." Vaguely Marxist.

It works unless it is "Pay 100% of what you have."

And yet, "Pay what you have" sounds a lot more egalitarian than, "Attend only if you can pay." Vaguely Marxist.

And as a result, we are encountering the bad outcome used in the classic critique of Marxism: there's no motivation to work. Or in this case, save.

Instead, why not just tax incomes in a fair and progressive manner, and use some portion of the revenues to provide quality higher education on a free or deeply-subsidized basis? The government could provide grants to prospective students (based on need), or, conceivably, could even set up its own network of "public-option" colleges.

54 That used to be the case, but these days some of the top private ones don't do that for folks in the bottom ninety percent or so. The trick is to make sure your kid gets into Princeton or Stanford and that you're earning under 150K or are so wealthy it just doesn't matter. Or you can do what my parents did - find an employer who pays tuition.

Seriously, 13, 51, 52, and 58 are exactly why I'm going 'lalalalalalala I can't hear you.' At our current incomes, saving more than the plausible sticker price of two college educations seems implausible -- we're not going to save to the point of having money left over when the kids have graduated. At that point, it seems really plausible that saving for college is completely pointless -- that we'd be better off with fewer assets once it comes to it. But this seems insane and irresponsible. And then I start cowering under my desk, whining softly to myself, alternating with the occasional pained yipping noise.

62: The trick is to have children at a young age. That way, you can save next-to-nothing before they're in college. And if all your kids are out of college by the time you're in your early 40s, you'll still have plenty of peak-earning-years ahead of you, which you can use to save for your own retirement.

Failing that, yeah, you're just fucked.

62 is us. Though, I suppose, when they shutter the UC, I could probably look for work at a hoity-toity private institution that does tuition swaps with other hoity-toity private institutions. That's a plan, right?

Some charts and tables to really cheer everyone up. Tuition inflation vs. general inflation (1.5 -2x, recently more towards the latter).

Failing that, yeah, you're just fucked.

I'm just fucked.

What's this "retirement savings" thing y'all are talking about? You mean like senior specials at the Red Lobster?

I agree with everyone else. Make sure you max out the 401Ks first.

I am so screwed about this because I have 4 kids and am not very frugal.

BU lets faculty and staff send their kids there for free. Harvard doesn't do jack.

MIT as well, although as of July I'm no longer an MIT employee, but that's ok because I have 13 years until the first one goes to school, by then I'll have moved up to custodial staff back at MIT.

What happened, SP? Do you have a a new job you like better or is your project just ending?

For our next financial planning discussion, is anybody considering long-term care insurance. I knwo somebody who almost dropped it, but now she's living in a glitzy place. Of course she can't leave for long to visit her kids in Florida. It costs her a $100/day and pretty quickly they start questioning whether she needs the help.

FWIW: We didn't do any saving. The eldest decided to go to a nearby State school and commuted (when she didn't spend the night). So I was out the cost of a car and the tuition. The youngest went to a private women's SLAC, which gave her a fairly good merit scholarship so the actual cheque I wrote each semester wasn't that much higher than if she'd gone to a public. They're six years apart, so we didn't have to pay for both at once. For both, we paid out of current income. Our cars aged. Our vacations were curbed. But it wasn't that painful.

It's very hard to plan around what's going to happen twenty years from now.

Still the same job, but we became an independent research institute. No more overhead to MIT. Much cheaper health insurance too (MIT is self-funded.)

Just to quantify things a bit here is my observations on the current shape of the landscape in the US for undergrad (this includes room & board which can run $8-11K).

National/well-known private Research Universities & "National" Liberal Arts Colleges: list price almost all narrowly clustered between $48-52K. "Very top" schools meet all financial need and have no school-based merit. Beyond these very select ones, varying amounts of merit scholarships are available, sometimes pretty significant, but there is increased use of loans and work study for "financial aid" and some do not guarantee to meet full "demonstrated need".

There is a bit of a gap then to more regional privates LAs and universities (often Master's only) which range in list price from $30K to low $40s. Almost all of these do merit aid and are mixed on meeting all demonstrated financial need.

Flagship and "first-tier" state schools. More variance here: from about $15-$25K in-state to $25-low40s out-of-state. Wide variability in merit & financial aid strategies--some give close to free rides to top students (sometimes just to those within the state) , some almost nothing.

A lot of the pricing strategies in the private university space (but not all) align pretty well with revealed preference rankings.

Harvard doesn't advertise its merit-based scholarships, but there's at least one for juniors. Incredibly competitive, of course.

74: Yes, that's more or less (though the numbers are a bit higher) what it was around late 01, early 02 when the youngest was looking.

Remember, though, that to a first approximation no-one goes to any of the "very top" schools.

If you poll the comments section here, I don't think that's true.

To a first approximation, no one comments here.

To a first approximation, Shakespeare's plays never got written.

"Very top" schools meet all financial need and have no school-based merit.

Those who are willing to settle for second-rate schools like Chicago or Caltech can get merit scholarships, though.

I'm thinking we can run a sale-leaseback deal with Newt and Sally. We'll sell 'em to the Guatamalan nanny and lease back possession, support obligations, and custody. The nanny will get the immigration advantages of having children who are US citizens, plus we can transform the ordinary income from nanny duties into unearned income from the leaseback, which wouldn't be subject to self-employment or FICA taxes. LB&B will get the advantage of excluding their resources when considering eligibility for financial aid, plus the kids would get minority preferences. We can patent the idea, franchise it, make a commission providing nannys, and bundle these sale-leasebacks into SIVs which we'll slice into tranches. Step 3: profit!

81: Knew I'd run afoul of someone with that characterizations. A few <insert your descriptor here> schools meet all financial need and have no school-based merit aid.

54: It's also egalitarian for the truly wealthy if you factor in donating to make sure Junior is accepted. I have a friend who gave $50,000 a year to his alma mater until his divorce, because he has kids (now 4 and 6). And look what Harvard did with the money!

When I was applying to medical school in the 80's, my adviser told me that it would be cheaper to have my parents donate $50,000 to get me into UCLA than to pay USC's higher tuition. I assume that if it was that obvious, everyone would do it, and a one-time $50,000 wouldn't cut it.

When I represented Caltech at high school fairs in the 90's, most of the serious questions I got were from parents about how to shelter their assets. Apparently your "competition" is thinking about this pretty seriously, and they are going to be able to afford to place their kids in good internships with the money they saved on tuition.

I keep wanting to write a longer response to 28.last, but can't quite decide what to say. I tend to agree with it, if all people are after is some credential they need for a job, or if their goal is just to learn a bunch of facts (libraries are wonderful places....). But there is a whole slew of experiences one can get a good university and nowhere else, and I'm not just thinking of the kind of cynical networking Cryptic ned mentioned in 34. On the other hand, if I tried to flesh that out, it might amount to saying "future and/or wannabe academics should attend the best schools possible." I like to think that all students benefit from learning from people who are actively involved in research, rather than just reading books, but it may not be true.

83: Aside from the fact that while she's of Colombian origin, she's now a US citizen, makes perfect sense.

85: And look what Harvard did with the money!

This week's installment: "Larry and the 6 Billion Dollar Endowment". Thank God no one important will ever listen to his financial advice again.

86: I do think that there is a relatively healthy piece of our current university system where most truly exceptionally capable and interested students* are identified at the secondary level (or early in college), and do end up concentrated in certain schools with great opportunities. They may be the minority of students even at those "elite" schools, but they truly are being apprenticed in the good sense of the word. Call it "Harvard (or wherever), the Good Parts".

*Not to say there isn't also far too much lossage that happens early on due to socioeconomic factors etc.

86: I think I know what you mean. I used to be a hard-line extremist on this, but I've mellowed a bit over the years as I've seen some of the non-narrowly-academic benefits of college that people can get.

These days I tend to frame my advice/opinions around what the end goal is. What are you going to college FOR? Night school and commuting worked perfectly for me, so I'm enthusiastic about making sure they stay open as possibilities in people's minds. But on-campus immersion at a very elite school was pretty much the only way that a few people I know could possibly have been educated in the careers they really wanted, so I don't want to dismiss it out of hand.

I guess the real thing I want to push back against is the idea that there's some magical incantation or set of rituals that upper-middle-class parents can invoke that will guarantee their child an elite job and high income. Not possible. The world changes. Teach 'em how to think and how to work and the rest is in God's hands unknowable.

90.last: I guess the real thing I want to push back against is the idea that there's some magical incantation or set of rituals that upper-middle-class parents can invoke that will guarantee their child an elite job and high income

Thanks for stating that so succinctly. And this a big chapter in "Harvard, the Bad Parts". The scandalously high graduation rates from those schools is one symptom.

I suspect 89 is rightish, but there's no reason that there should be such a gulf between the top schools and the rest.

And of course university education should be free; this idea that by rather stupid means testing you get a good result is bizarre.

And of course university education should be free

I agree. But in the US, this is unlikely to happen anytime soon, so I would pile on with advice that parents should probably feel okay asking their kids to contribute. My own parents made it clear they'd cover tuition and a free place to live (their house). If we wanted to go elsewhere, we had to find the scholarship money to do that.

I did just that, paying for room and board on a hodgepodge of random scholarships; my brother chose to live at home for free and go to a school closer to home. And there were no hard feelings about this arrangement.

Oh, and books were also on me. So I waited tables during summer and on breaks, saving up roughly $800 for a semester's worth of books and spending money.

Oh and I went into mild credit card debt (roughly $1000) going to study in South America my third year. Free and clear now, but I suspect that sort of thing is common.

And there were no hard feelings about this arrangement.

Au contraire. I'm still mad at your folks for not giving you a full ride.

We hate that fr/end of yours as well, son.

Loans taken out by the student seem to be getting short shrift here. Per 74, "meet all financial need" includes a hefty helping of those, unless I'm totally out of date. I met roughly those criteria - parents had no assets to speak of (my dad didn't become a homeowner until I was out of undergrad), but managed to pay my room and board, and the school met my financial needs with something like a 60% grant/40% loan mix. I know a few people who ended up pretty much getting loans for 100% of their undergrad education at high-end schools (usually because some kind of divorce mess scrambled the aid calculations); this seems like it was a bad idea for them, as they're still making huge payments a decade later. Faced with that situation, state school would have been a much better idea.

96: Mmm. I will feel very bad about myself if my kids come out of undergrad with serious student loan debt. OTOH, if they need student loans to make it through, I suppose we can always make the payments for them afterward.

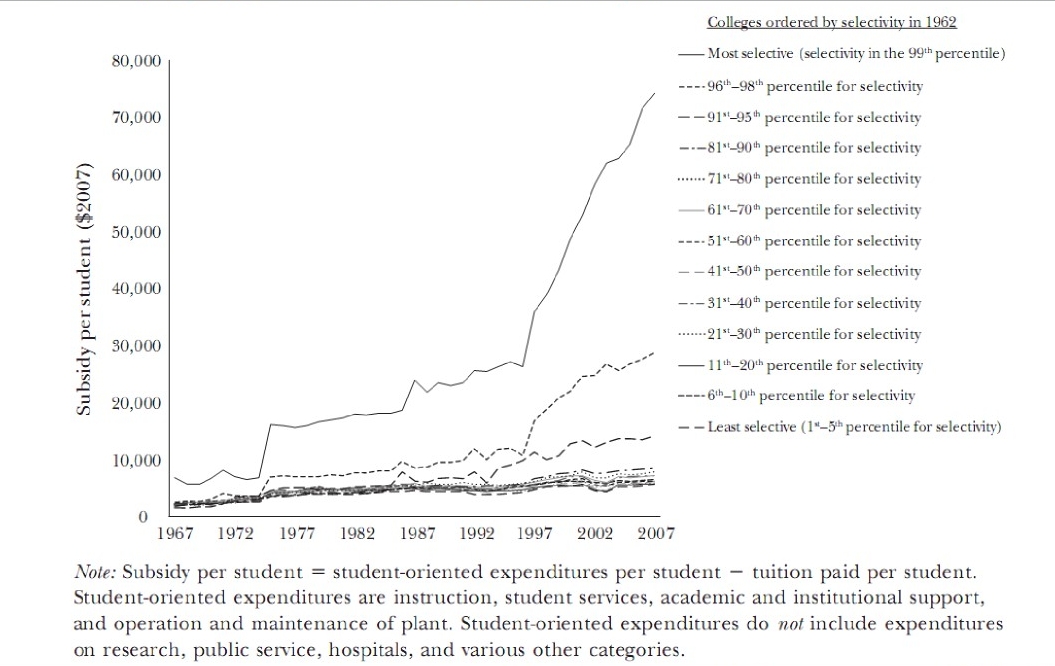

97: Yes, I almost linked that paper (and would love to read it, but not sure $5 worth). Given this line in the abstract, An important finding is that, even though tuition has been rising rapidly at the most selective schools, the deal students get there has arguably improved greatly. The result is that the "stakes" associated with admission to these colleges are much higher now than in the past. , I wonder if it was the source for a great graph that I saw recently (and frustratingly cannot find, I thought it was in the Times) which showed the actual expenditure per student over time. What it showed was an astounding run-up in the past decade in the expenditure by the school per student at the most selective schools (the very few, very wealthy ones which augment tuition with other income).

99: So the "deal students get there" means the size of the college's budget? Not the future success of the students?

100: Thanks. And yes that was the source of the graphs I saw. Found one of them online here.

101: In this case sorta yes, they define "subsidy per student" which is "student-oriented expenses" minus tuition. If you look at the graph I link above you will see that it is quite the story. Basically it shows the "subsidy" at the top 1% of schools measured by "selectivity" at over $70,000 while schools below the top 90% were clustered between $5,000 and $10,000. The difference grew rapidly starting about 15 years ago. It is quite telling. Also relevant is this Randy Cohen column from a couple of month's back, "Should You Give to Harvard?"

{kind=link}