... I'm not finding a good summary to link to ...

Felix Salmon linked to this a few days ago. Don't know how good it is.

it seems to be that the people running the incredibly profitable mortgage securitization businesses were overwhelmed by the volume of paper they would have had to process to do it properly

Well, going through the paperwork process would involve delays of weeks, which would slow down the land-flipping activity that was the cause of the profitability in the first place. Even if they paid enough people to process all the paper, actually going through the process would slow things down to the point that people would start to question the money involved and then the whole Rube Goldberg contraption that was the housing bubble would collapse.

Thing is is that hinky paperwork is a feature of every real estate boom - I know they were doing it in Kentucky back in the early 1800's (which was part of the problem of making Kentucky a state - when they went to survey all the land they discovered a lot of bad land titles) and they were still doing it in Texas during the S&L boom/bust.

Invent a new line of business that's incredibly profitable,

They aren't incredibly profitable without the fraud though. Without the fraud a lot of this stuff is actually a money loser. That's why financial innovation is bullcaca. The innovation is just coming up with ways to make meaningless paper look valuable. Kinda like the way Zynga makes money off of Farmville: nothing is actually happens, but it sure looks like something is, and that's where the money is.

max

['Same as it ever was.']

2

They aren't incredibly profitable without the fraud though. Without the fraud a lot of this stuff is actually a money loser. That's why financial innovation is bullcaca. The innovation is just coming up with ways to make meaningless paper look valuable. Kinda like the way Zynga makes money off of Farmville: nothing is actually happens, but it sure looks like something is, and that's where the money is.

There is a lot of truth in this. At the moment the mortgage market is almost entirely supported by the government because no rational investor would loan on current terms.

At the moment the mortgage market is almost entirely supported by the government because no rational investor would loan on current terms.

I'm wondering what this means. In fact, lending is going to be constrained in the current economy because people can't afford mortgages for a variety of reasons.

2 shouldn't be so surprising to me, because I remember being amazed more than a decade ago when I found out how long it took to get the final paperwork after settlement. I just couldn't understand how it could take the bank and the county registrar of deeds so long to process something that seemed relatively straightforward.

It's kind of stunning to realize that the investor's solution to this is "Then skip it!", though.

This is less level headed than the Financial Times piece, but it does contain lots of stories about the human costs of the shoddy paperwork/fraud.

It also makes some really alarming claims, like that it was standard practice in Florida to shred the actual paper mortgage once an electronic record of it was established at MERS, and that 95% to 99% of the foreclosures in FLA are fraudulent.

I have a copy of my mortgage in the files at home. It says they have to give me a pony after 7 years of on-time payments.

At the moment the mortgage market is almost entirely supported by the government because no rational investor would loan on current terms.

This basically is back to front.

I remember a story or two related to this from way back in 2008 or so - some people were getting around foreclosure and staying in their homes by simply refusing to sign anything away until they saw the proper paperwork, and it was working, at least so far. Back then it was presented as a "lighter side of" the financial crisis, a joke and/or an unpredicted ray of hope.

I wonder if any of those people are still in their homes. Probably not. Capital one.

4

I'm wondering what this means. In fact, lending is going to be constrained in the current economy because people can't afford mortgages for a variety of reasons.

In a free market housing prices would fall to affordable levels. But the government doesn't want that to happen so they are giving people mortgages they can't afford. See for example this NYT article (a year old but I don't think anything has changed).

"I knew in my heart I could not really afford the house, but they gave it to me anyway," said Mr. Fullenkamp, 22. "I thought, 'Wow, I'm surprised I pulled that off.' "

This legal analysis was linked to on one of the mortgage finance blogs. It seems that using a shell company (MERS) to avoid paying the fees for assigning a mortgage has consequences...

This basically is back to front.

There is no way I'm going to see that movie.

2 3

My thoughts on the true value of this "new line of business" can be found here and here .

As for links, the WaPo has had a series on the foreclosure mishegas, including this one about MERS and a graph with arrows (I like graphs).

9

This basically is back to front

The intended meaning of this comment escapes me.

15: I do too, but that's kind of a shitty graph.

It's kind of stunning to realize that the investor's solution to this is "Then skip it!", though.

Well in this particular case it wasn't so much the investors' solution (except insofar as they didn't dig too deeply into individual loans). The securitisation documents contain legally binding representations and warranties from the sponsors saying that, among other things, the loans were originated and transferred in compliance with applicable laws. Sponsors have to buy back loans which are found to be non-compliant. The problem is a) many sponsors are now bankrupt, and b) it involves a lot of forensic work to go through each loan and prove non-compliance. So far only huge investors like Fannie and Freddie have been doing it en masse. The recent revelations (which aren't really that recent if you'd been following Naked Capitalism or the late Tanta's posts on Calculated Risk) suggest that repurchase requests are going to be much, much more widespread.

This could very easily become a second crisis with hundreds of billions of dollars in losses for banks, but I suspect that the government will fudge the invalidity of title issue. My guess is that banks will be forced to repurchase many, many loans, but they won't take a much bigger hit on them than investors would have done absent the title issues. Which could still be a very big hit indeed.

Jail and/or hang. Pour encourager les autres ... innit.

18: Insofar as I understand it, there's a dual problem: first, the technical invalidity of title due to failure to properly transfer the documents, and second, a substantial loss of actual information about the terms and ownership of many of these loans because of the failure to maintain the original documents. The first, while it's a mess, can be fudged by government fiat, and that's probably the right thing to do on some level: if you've got a loan with known terms, and a contractual trail establishing who paid for it in the end and therefore who it should have been legally transferred to, there's no equitable reason I can see not to go back and fix it. The second is a stickier problem, and finding out how much of that there is will be really laborious.

The first, while it's a mess, can be fudged by government fiat, and that's probably the right thing to do on some level:

Probably, but I'm still pissed that TARP was done in such a way as to help big banks without requiring anything new of them. I'm guessing that I'm not the only one who thinks that and that there will be a big political cost for any fix that seems tilted in favor of banks.

Of course, there will be a lame duck Congress in a few weeks. Fuckers will do it then.

that's kind of a shitty graph

Perhaps you prefer today's graph, which, among other things, suggests how completely forked the Florida housing market is.

But of course allowing cramdown on primary residences would destabilize the nation ... unlike allowing it on secondary residences.

The asymmetry of moral hazard assessment--contributing symptom #137 to my late-empire fatalism.

I am saving the world economy.

You are cutting corners.

They are deadbeats.

Mike Konczai's blog has a five part series, after which you'll know more about it than the banks.

Also, my link stash on the issue is here.

I'm a bit nervous about how scope of the consequences as I am a couple of weeks into helping a family member work through the sale of their residence (have an accepted offer). In this case there was a refinanced mortgage with WashingtonMutual that then became part of Chase (I presume as part of the sale) and then last August the owner received a letter saying Fannie Mae had taken ownership (or something, forget the precise words and don't have the paperwork in front of me) but that Chase would continue to service the loan. Presumably in a sale (and this property is fortunately way above water) as long as the servicer Chase gets the dough, it should be OK and they will close it out, but I still fear specific documentation problems or general financing issues on the other side due to the debacle.

after which you'll know more about it than the banks.

Not too hard, apparently. But those are excellent articles, you beat me to the recommendation because I was reading them.

how completely forked the Florida housing market is

The Florida housing market has many bifurcations?

This basically is back to front.

There is no way I'm going to see that movie.

100% off topic, but there is now a big budget porn parody of The Human Centipede called The Human Sexipede. You can find the trailer easily enough via google (it's hosted on Fleshbot, but I'm at work), and it's actually pretty funny and not gross.

In this case there was a refinanced mortgage with WashingtonMutual

Uh oh! WaMu screwed up my depositing a check in my bank account (they put it in someone else's and put someone's ISF check in my account and then charged me). I had all the documentation in the world (including the bank statement and canceled check [marked as deposited in my account!] from the friend who had written it to me) and WaMu had none. This did not stop them from fighting me on it for quite a while (they even did an "investigation" which showed, against all evidence, that they acted correctly), until I pitched a truly epic fit. And even then, I only succeeded because I had a bunch of documents people really can't be expected to have (the bank statements and canceled checks of other people).

...Huffington

Some jurisdictions such as Baltimore toss in unpaid water bills and other municipal fees of $250 or more. In May, the Investigative Fund reported how an unemployed former mental health counselor with four children named Vicki Valentine lost her home even though the mortgage had been paid in full. She had owed $362 on an overdue water bill when investors took over and added thousands of dollars in legal fees she couldn't afford. (In response, city officials are seeking statewide legislation that would prohibit the sale of tax liens of less than $750.)

The big banks have the resources to always and immediately find a new "profit center." They are an imminent threat to economic and political stability, and already have done damage that is irreparable.

Politics and the law are not on the side of the good guys, and cannot be until the power is redistributed. I think we need to organize a national debtor and taxpayer strike, protect possession by any means, and bring the jubilee.

And I am not voting this year.

18: Also, if loans weren't properly transferred from a now-bankrupt entity, not only can the securitization trust not put them back, but they also can't have them properly transferred to themselves now, because these trusts aren't permitted to acquire title to assets after their original closing. There's no way the outcome of that is going to be free houses, though.

27: I'm very glad not to be in the title insurance business.

Tell Vicki Valentine the system works, will work. Tell her the lawyers are on her side.

The post, which seems to be simply demanding the banks hire more and more expensive lawyers, sucked.

There's no way the outcome of that is going to be free houses, though

I know, deep down inside, everyone is thinking this. "Maybe if the paperwork is too fucked up, they'll just give me my house!"

Unfortunately, the reverse outcome is more common. The WSJ apparently has argued that this isn't a big deal, because we can "only" confirm seven cases where people have been unjustly thrown out of their homes.

31: WaMu--they dead. At least. But you are right it does not add to the confidence.

I had a somewhat similar story with a local bank (and one tightly associated with my father's employer) from way back in college. Someone got hold of my bank account number and fraudulently took out a few hundred bucks. I was away at school and not checking statements too closely (i.e. at all) so I only discovered it a few months later when I ran out of money. I got the money in the end, but a big fight with investigations--where were my roommates that day? etc. What irked me was that they had clearly done no due diligence at the time--signature was not at all like mine, and they got some info on the withdrawal quite wrong such as the spelling of my street. The bank kept pointing to the fact that they had been "complex" transactions, something like taking $400 out of savings and putting $100 to checking and taking the rest in cash, as if that level of minimal cleverness and misdirection were beyond the capability of a criminal.

dsquared bait, Lizardbreath?

37: Not particularly -- I'd probably have done some more background reading if I'd thought I was going to have to argue with him about it. Has he been posting about this someplace?

I'd probably have done some more background reading worn my abestos underwear if I'd thought I was going to have to argue with him about it.

I change my underwear for no man.

Wait, that sounds bad.

I wear assbestas underwear. They make my ass look best as it can.

Also, if loans weren't properly transferred from a now-bankrupt entity, not only can the securitization trust not put them back, but they also can't have them properly transferred to themselves now, because these trusts aren't permitted to acquire title to assets after their original closing.

I'm not an expert on the US situation, but my understanding was that they could, but they'd lose their Remic tax status. Again, not an expert on US structured finance, but I'd have thought losing tax benefits would be better than losing your entire collateral.

have thought losing tax benefits would be better than losing your entire collateral.

I'm really talking out of my ass now, but I wouldn't be surprised if they were equivalently bad, in that losing the tax benefits would be enough to make them insolvent.

If I could talk out of my ass, staff meetings would be something I looked forward to.

46: Whereas your coworkers would likely just look away.

Not that silently farting while everybody looks around is worthless, but one does long for variety.

There seem to be a good many lawyers here, so, you know, probs someone can answer this:

If there are potentially or probably a large number of people who are being forced out of their homes fraudulently (also known as stealing? that's what they're doing, right? stealing?), is this the sort of situation that might lend itself to a class action suit? Because if a bank was coming after my home fraudulently, I'd wanna sue. I also probably wouldn't have the resources to go up against their legal departments. This is what class action is for, kinda, right?

I want Glenn Close to take the case. And Rose Byrne. Reeeeeeallly want Rose Byrne to be involved somehow.

I know the question was already asked, but can someone point to a good summary of the situation? Most of the journalistic accounts I've read are incredibly confusing (and confused) and it's hard to figure out what's OMG SCANDAL from the actual scandal.

Personally, I recall falling asleep during the part of the bar review course that covered transfers of title to real property. So boring! So I guess I would have been qualified to work at a bank.

50.2: The rest of the bar review course was engrossing?

49: Mmmmmaybe? That is, I don't know for real, but it doesn't seem implausible at first glance.

49.3 I am definitely cool with more Rose Byrne on unfogged. Just in case you're looking for lesbian consensus. I am not good at having celebrity crushes because so few celebrities seem like they'd be fun to talk to, but I think she'd be great fun and we could be friends and have zany adventures and so on.

49 -- There are a couple of AG led class actions going on.

Halford, there are a bunch of different things going on, but one significant strand is that when mortgages were collected and securitized, the people doing it didn't keep track of the original paper, instead relying on electronic data. In a world where foreclosure isn't going to happen -- a world where values are always rising -- this isn't that big a deal: a homeowner in personal trouble can sell the house he can't afford, and downsize with the equity into something he can afford. (Or borrow against the equity to tide over until the personal problem is passed).

We don't live in that world. Instead, we live in one where foreclosure happens, and where courts want to see the original signed documents, not just printouts from databases. One response, apparently popular in Florida, is to make up affidavits from people who say they saw the documents, and this is what they say. Then file fake affidavits of service, so you can do the foreclosure unopposed.

Over at the other end of the thing, the investors who bought the securities were promised that the sellers of the securities had all the documents, and everything was fine. They didn't (in a non-trivial number of cases) and so there's a rep and warranty issue.

I don't doubt that there are a bunch of erroneous foreclosures going on: banks have wrong addresses, payment records are screwed up, and the like. I personally think this is going to be in the low single digit percentage of foreclosures -- obviously to the affected homeowners, it's 100% of foreclosures -- most being actual cases of default.

But even where there is a default, there is a standing issue -- who actually has the legal right to foreclose -- and the proof issue.

49: This is my business. We're looking into it. Anyone whose home was stolen probably has enough at stake to bring an individual case, not a class action. It is also likely that there would be individual cases in any of those cases. And we certainly hope that the instances of fraudulent foreclosure (where the individual is not behind on payments) are few and far between.

We're looking at possible class cases for people whose mortgages weren't properly recorded, to get back the part of the closing costs that was supposed to pay for getting the documents correctly recorded. We also have some interesting cases on price fixing in closing costs, against title insurers and banks.

There are also lsots of cases involving investors in those securitizatiosn, but the clients ar einvestors, not homeowners.

5: It's kind of stunning to realize that the investor's solution to this is "Then skip it!", though.

I got stunned back in the 80's by the S&L thing. The second time through just breeds cynicism. But the answer is always and everywhere, 'They were going to unload the property on the next sucker before the music stopped.'

4: I'm wondering what this means. In fact, lending is going to be constrained in the current economy because people can't afford mortgages for a variety of reasons.

Shearer's talking about the crappy interest rates on offer. Why make loans for 1% (or whatever) in returns when you can invest in the stock market? Or bonds. Or Brazil, really.

They had a story on CNN I think, with a bunch of old people complaining that they weren't getting any interest on their CD's now so they were having to unload their capital, and they were afraid of running out of capital before they died. Thus, they wanted the Fed to *raise* interest rates. And ya know, fuck the unemployed.

18: My guess is that banks will be forced to repurchase many, many loans, but they won't take a much bigger hit on them than investors would have done absent the title issues. Which could still be a very big hit indeed.

I'm guessing that's why Treasury seems unable to do anything about the issue. They'd do anything to avoid killing the banks a second time. Of course, that makes them look like shills. Which they are, in this case, for good reason. The banks won't get bailed out a second time, so if they start to sink, uh oh.

max

['We coulda had a cramdown session, but we get healthcare instead.']

One thing that really surprised me was the shoddiness of the court proceedings for FL foreclosures.

Taking something that doesn't belong to you on hte basis of botched paperwork, is that really fraud? I thought that definite intent was a necessary component of fraud, and that setting up a distributed shambles so that there is no single decision-maker is indeed an effective defense (de facto defense, not de jure) from any sort of punishment, beyond fines.

One obvious target against whom there should be a fraud case (countrywide sold securities they characterized as shit in internal documents to investors without informing them of problems) is apparently getting away with a fine equivalent to 1 year's compensation and a tiny fraction of losses caused to investors, no admoission of wrongdoing.

http://www.nytimes.com/2010/10/17/business/17trial.html?_r=1

we get healthcare instead

Maybe, but I wouldn't bet the mortgage on it.

Alex's link in 26, which I missed before, is really excellent. I especially like the graphs -- it's a good example (useful for lawyers!) of how to convey complex information coherently.

It's still not totally clear to me how precisely the contracts between the sponsors and the trusts work, and how the buy-back provisions can be invoked (which seems to be the point at which this goes from "extremely troubling and dubiously legal actions by banks and law firms" to "holy shit total financial meltdown and lawsuit bonanza"). It would be interesting to know how standardized such contracts are and how insulated the big remaining banks are from the buyback provisions.

Brazil

Not possible for retail investors, I think.

Buyback provisions

So far lawsuit bonanza and victory of the biggest, I think.

http://finance.yahoo.com/news/Judge-Dismisses-Class-Action-law-480481740.html?x=0&.v=1

Well. It does seem there will be plenty of work for lawyers.

Reading stories like this, and then like this:

sometimes make me regret having such a functional empathy center. (That's a thing, right? Empathy center? Really large in elephants?)

Really, life is probably much easier if you don't give a shit about anyone else, or morality, or ethics. Like, waaaay easier. I'm sure Glen Beck, for example, sleeps like a baby.

55, 58 - The mortgage courts in Florida honestly come off worse than the banks, imo; at this point, I expect banks to behave illegally, but it's amazing that the bulk of the special court judges just rubber-stamped foreclosure proceedings for institutions that quite evidently didn't have legal title to the houses.

Unimaginative though he may be, I'm sure our friend will figure out a way to get appropriate authorization to file his suits. That avoids 61.last.

"I'm guessing that's why Treasury seems unable to do anything about the issue. "

There's a limit to what Treasury can do, not least because foreclosure law varies massively from state to state. Plus, at the securitisation level, you have contracts which Treasury can't repudiate. Of course, if the FDIC takes BofA into receivership, all bets are off, though it claims it will honour existing securitisation contracts or pay damages.

64 -- Nothing that happens in a Florida court would shock me. Well, almost nothing.

Yeah, "Florida courts are terrible" is about the least shocking news in the world to anyone who has ever spent time in them.

61.last: It can be hard to know who to cheer for in some of these cases. In that one, I suspect Greenwich Financial Services Distressed Mortgage Fund 3 LLC is the worst kind of bottom-feeding fund--and they were pissed off that some mortgages had renegotiated lower rates. But of course who wants to defend Countrywide?

There is only one rule--there are no rules, except no person of upper middle class status or "higher" shall suffer any significant loss of status.

It's overcast and I had a really bad day yesterday, so I'm gonna keep talking about Rose Byrne. (Hi Thorn!)

I, too, find her visible dread of the red carpet to be endearing.

http://gofugyourself.celebuzz.com/go_fug_yourself/cat_1141/

59: Maybe, but I wouldn't bet the mortgage on it.

We already have.

61: Not possible for retail investors, I think.

You can buy into emerging markets funds and the like without getting into the Brazilian stock market. It would probably beat parking the money in a 0% interest CD.

66: There's a limit to what Treasury can do, not least because foreclosure law varies massively from state to state.

I almost said the Obama administration but that didn't sound quite right. USG could have acted on the mortgage issue for reals back in 2009, but instead we got HAMP. The administration tried to prop up housing prices just like elite opinion thought they should. Unfortunately.

We could have and are (finally) having Fannie and Freddie buy up all those mortgages a lot sooner than we did (as JP noticed above), which wouldn't have straightened out the paperwork but it would have stopped the sharking involved in all the foreclosures that have already gone down. It would also have shored up the banks a lot and pumped a lot of money into circulation. They finally did that but only after a year of waiting.

Now we have the banks running around trying to "solve" the issue and the administration is standing there with their hands in their pockets and it looks like they're favoring the banks. And they are, both for good and sensible reasons of financial stability and because there isn't much they can do without Congress, but it still looks really crappy.

max

['GAH!']

IANAFL (or a FLL) but it seems to me that the proof and standing problems can probably be solved, even without federal/state intervention, although this would raise the cost of a foreclosure action considerably.

Problems within the system (ie, not between borrower and lender, but between various players on the lender side) seem a lot more difficult, since so many entities who bear ultimate liability have disappeared.

You can buy into emerging markets funds and the like without getting into the Brazilian stock market. It would probably beat parking the money in a 0% interest CD.

You should probably not invest money you need to live in the Brazilian stock market if you are past working age or nearly that old. A CD might pay 0%, but a security can pay anywhere down to minus 100%. Patients who smoke should consult their doctor before investing in Brazil. Close cover before striking. Results not typical. Consult your doctor's golf buddies.

I, too, find her visible dread of the red carpet to be endearing.

Me, too. Sometimes seeing usually-hidden emotions in public faces reminds me of the story about Kurosawa picking Toshiro Mifune out of a cattle-call audition because the director saw through the blustering, angry punk act that Mifune was putting on to cover his nerves, which when you think about it is sort of an odd recommendation for a movie star. It worked out OK, though.

Am now looking at the Fannie Mae letter the only part that seems potentially kind of odd is, "The transfer of ownership of your mortgage loan to Fannie Mae has not been publicly recorded." That is probably correct for some technical reason--just not sure what to make of it.

75: It means John Stamos owns the house now.

I just got a similar Fannie Mae letter from Citibank, and am trying to sell my home. I don't have it in front of me, but it seemed to indicate that I should just continue to work with Citi for both regular payment and/or any closing out of the loan. It still makes me nervous.

76-7: Unfortunately, Dave Coulier lives there too, along with one of the Olsen twins on an alternating basis. And you have an annoying neighbor girl.

79: Great, I'll be there tonight. Par-tay! That's how you kids say it, right?

See for example this NYT article

James, your example seems to prove the exact opposite of what you claim it proves. In fact, the FHA's role here is to make it less costly for lenders to lend, by insuring buyers. Ask any libertarian: When the government intervenes to subsidize an activity, you get more of it.

Is this good public policy? Has the FHA behaved wisely in carrying out it's mandate? I dunno. But that's not the issue you raise. Remember, here's your claim:

At the moment the mortgage market is almost entirely supported by the government because no rational investor would loan on current terms.

The example you provide renders this into gibberish. The government is supporting the market and therefore supporting the lenders.

funds

equities are pretty easy ( many trade as ETFs), I thought real-denominated bonds were intended.

81: I think you've got Shearer's claim flipped -- he seems to be saying the same thing you are, that the government is supporting lenders, and in the absence of that support they'd have less incentive to lend.

81: The government subsidizes lending, making more of it available. Without support for the lenders, lending would be much more expensive than now. Given that all cash buyers are very rare, the price of housing is set by the amoung of debt that can be serviced on a given income. In other words, the government is both supporting lenders and keeping house prices up.

(on preview, pwned. But I don't see what your beef with Shearer is in this case.)

the government is both supporting lenders and keeping house prices up.

Someone decided a long time ago that home ownership was good public policy. Stakeholders and all that. Unintended consequences: lack of mobility in a down market, which is when workers need to be more mobile. Just an other distortion of the market brought to you by government intervention.

73: You should probably not invest money you need to live in the Brazilian stock market if you are past working age or nearly that old. A CD might pay 0%, but a security can pay anywhere down to minus 100%.

Nonetheless there's the lure of returns.

82: I thought real-denominated bonds were intended.

Nah. I'm thinking either hot money chasing returns or silly people, which most retail investors seem to be these days. Both can (will!) stick with dollars.

If the retail investor types really want out (sensibly or not) they'll probably buy gold or something.

78: It still makes me nervous.

I'd think it would make you feel more secure. You're in the loving arms of the government, so getting surprise foreclosed is unlikely.

max

['GSEs are your friends.']

they'll probably buy gold or something.

No better example of greater fool theory. Personally, I'm investing in canned goods and ammo.

Copper is inherently useful. I think I'll invest in copper statues of myself. Attractive and salable!

No better example of greater fool theory.

The gold thing is just so bizarre. If the entire economy collapses, how much gold can you eat?

McMegan channels George Bailey as to why a cramdown is a bad thing

There are periodic reports of widespread copper hoarding in China now, where stock markets are worse regulated than here and property is in a bubble, so there's notionally no good way for people there to save their money. In the late 70's, many people in the US turned from equities to commodities as something tangible, and created bubbles in the prices of many kinds of food.

Gold makes some sense if you expect inflation rather than collapse. It's also a portable store of wealth, and would be a way to start over in another country or with revalued currency. Savings confiscation through inflation has happened many times in the 20th century, though not in the US. Thinking about unlikely disasters usually makes people stupid, though.

Thinking about unlikely disasters usually makes people stupid, though.

And the rest of us were stupid to begin with.

If the entire economy collapses, how much gold can you eat?

Is that a challenge?

93: Brock wins. Well, Brock and his baby.

That would be a Pyrrhic victory indeed.

There are periodic reports of widespread copper hoarding in China now

Is the US military looking into deploying armies of thieving tweakers?

95: Only a fool would accept that challenge?

There are periodic reports of widespread copper hoarding in China

Before CoinStar, there was widespread copper hoarding in my house.

Before CoinStar, there was widespread copper hoarding in my house

I use these, but choke on the fee. 10% is a lot to pay for laziness.

100: There's no fee if you take it in Amazon gift cards.

Coin-Star? I keep change in a jar, and when the jar is full I put the change in paper sleeves and carry a big heavy bag of metal to the bank and deposit it. Call me old-fashioned, but I probably do that an average of once a year (the last time I did it I ran out of a certain kind of sleeve, so I had to get more and make a second trip), and it doesn't seem too hard.

Cool! Not only amazon, but a bunch of retailers, like Starbucks and itunes!

Probably not, pennies stopped being copper in 1983 and melting them was made illegal a few years ago.

Hoarding valuables is a common response when people lose trust in the banking system. Bank failures don't lead to starvation or to fighting in the streets, but they are very hard on the comfortable middle class. Argentina, Thailand, and Russia all had this happen in the 90s. It's easy to snicker at people who get wide-eyed and excited about apocalypse, much harder to think through reasonable contingency plans.

For myslef, I'm anxious, it's hard to figure out how much to worry about some larger crisis. Zero is wrong, but retreating to a farm seems extreme. Gold does indeed look really expensive now, and so does everything else.

As for myself, I'm heavily invested in self-delusion.

Gold does indeed look really expensive now, and so does everything else.

New York state wine in a box is pretty cheap.

Probably not, pennies stopped being copper in 1983 and melting them was made illegal a few years ago.

There's still copper on the outside and melting pennies is less illegal than melting your neighbor's plumbing.

All my money is invested in unfogged.com.

My parents tried to buy a house recently and were thwarted at the last second by a title search coming up with a still existing mortgage from several years ago (prior to the current "owner") owned by a no longer existing mortgage company. Sale fell through. Now that house is basically worthless and un-sellable all because somewhere along the line people didn't correctly deal with paperwork. And it's only a $40K house, so the cost of hiring lawyers to deal with the issue and paying off some of the creditors of the mortgage company leaves little in the way of options. Hopefully the current owner has some sort of title insurance from when they bought the house in the first place.

Had I been savvier, I'd have invested in a stockpile of Tostitos Gold™, because, man, those were delicious and now you can't find 'em anywhere.

83 and 84: Yeah, either you or I are misreading the phrase "on current terms." I thought that James was blaming the government for the lack of lending, and suggesting that there would be more of it were it not for government interference. In my reading, the "current terms" he discusses are the terms that lenders get under the government-influenced status quo.

Can you clarify, James? Why is nobody lending on current terms?

111: By current terms, I assume he is speaking of the interest rate/down payment/fixed for thirty years terms of the loan. That would be how "terms" is used when talking about a loan. Just politically, nobody libertarian is making the complaint you think Shearer might be making (except possibly as a "years down the road" kind of thing).

110 - I know. Greatest lost to the American snacking public since Trader Joe's discontinued the Chinese mustard fried wonton wrappers.

A friend of mine lives in Norway and every now and then she sends us a bag of Bugles Dipped In Chocolate. These are fucking amazing and you should stock up if you're ever around them.

How hard is it to melt chocolate on a Bugle? Don't let Norway continue its drive to mechanize all that is good in life.

But, now I have the best fondue idea. Thanks.

I suppose you could just buy Magic Shell and dip bugles into it. But Magic Shell always tastes like plastic.

Or fondue. You say fondue-toe, I say Magic Shell-o. Whatever.

You can melt chocolate, whatever kind, using things you probably already have in your house.

All you need is a glass bowl, some chocolate, a zippo lighter, and some books to keep the zippo from tipping over.

You could probably use a cat, if the cat had a fever.

You can melt chocolate, whatever kind, using things you probably already have in your house.

You can make a decent breakfast using things you probably have in your hotel room.

112:

Just politically, nobody libertarian is making the complaint you think Shearer might be making

But James isn't just any libertarian. Here, he seems to be specifically concerned about the government's influence on the "current terms."

Let's rewind the tape: When I (in comment 4) sought clarification of James's original point (made in comment 3), he offered this (in 11):

In a free market housing prices would fall to affordable levels.

My 81 was a response to 11, which was written to illuminate the content of 3. In 11, James illustrated his point by linking to an NYT article about the FHA - a government entity that (in James's narrative) is making housing prices unaffordable. Not merely higher, mind you, but more unaffordable.

Alas, many great thinkers are obscure to the lay reader, and I hope I can be forgiven if I've gotten James wrong on this. If only there were some way to resolve this conundrum ...

And no, I don't have anything better to do. Why do you ask?

102: I keep change in a jar, and when the jar is full I put the change in paper sleeves and carry a big heavy bag of metal to the bank and deposit it.

The tellers at the banks I deal with much prefer it if you just keep it in a bag, unwrapped. Because all they do with it is take it around to the back and put it through a coin-counting machine, so it's a hassle to take it out of the rolls.

I think the local crappy bank (TCF -- not googleproofed, because everyone knows it's a shitty bank) actually charges you to deposit change, as well as having a CoinStar, or clone thereof, in its lobbies. Real banks to not seem to charge anything.

What I'm curious about is, would gold actually be a currency in post-apocalyptic or anarchic times, or is that just an assumption we make because it's associated with the olden days? Do they use gold in Somalia, say?

I guess the hardest currency in practice in Somalia and places with bad national currency is the dollar, so that's no help.

I guess the hardest currency in practice in Somalia and places with bad national currency is the dollar, so that's no help.

Do the pirates use those little highlighter pens to check if the ransom money is legit?

||

rather interesting speech by Jon Crudas [perhaps more for the British readers]

>

All you need is a glass bowl, some chocolate, a zippo lighter, and some books to keep the zippo from tipping over.

And here I am all outta weed.

Two friends of mine own not-insignificant amounts of gold bullion, for reasons that they've never quite expressed.*

* Thunderdome.

110: Had I been savvier, I'd have invested in a stockpile of Tostitos Gold™, because, man, those were delicious and now you can't find 'em anywhere.

Damn. I hadn't even noticed the loss, but now that you bring it up, I really feel it. Where are the Tostitos of yesteryear?

134: They're planning to usher in the Minestrone Age.

131: I think you might want to ask Stanley.

||

I sometimes wonder whether my employer's practices aren't bad in the same way, though not to the same degree. There's an awful lot of backdating--where someone says that a treatment plan was written before it was etc.

Nobody's getting a ton of money for phony surgeries, and there's a lot of work that goes uncompensated, but I still think that it's technically me/dic/aid fra/ud.

|>

125

What I meant is that you can currently obtain mortgages on irrationally generous terms because the government is subsidizing them. This is likely going to cost the government a ton of money and is not really helping the buyers much because they are paying an inflated price.

On the other hand, it does wonders for refinancers.

139

On the other hand, it does wonders for refinancers.

And for the banks whose bad loans are being replaced with new bad loans but with the government on the hook for losses.

Well then, can we all agree that the government is subsidizing buyers, sellers and others who benefit from transacting in homes, including lenders?

Like Bush and Obama - but unlike Sarah Palin and the Tea Partiers - I'm a supporter of TARP (assuming the choices are TARP or nothing.)

Moneyed interests really have taken the economy hostage, and while I think there are ways to make the ransom cheaper, that ransom has to be paid. If a soft landing isn't found for the housing market, we're really fucked. (I mean really fucked, as opposed to the fucked that we are anyway.)

And for the banks whose bad loans are being replaced with new bad loans but with the government on the hook for losses.

I'm not sure I get this. Any bad loan that gets refinanced is a loan that may well otherwise have defaulted completely.

To the OP: Isn't this a race-to-the-bottom problem, once the players notice that whatever rules there are aren't presently being enforced? Hire a couple of cheap, junior lawyers and you're now going to lose out to the entities that don't even bother to do that.

142: Yes, and if the loan was made during the boom, the loan may be privately held. Nearly all of the new stuff is government. Refis have helped private banks diversify and raise capital and if the housing drop continues will cost big government money.

141

Moneyed interests really have taken the economy hostage, and while I think there are ways to make the ransom cheaper, that ransom has to be paid. If a soft landing isn't found for the housing market, we're really fucked. (I mean really fucked, as opposed to the fucked that we are anyway.)

Why exactly should the government be spending hundreds of billions of dollars propping up housing prices.

@130: Romero! Polanyi! Bevan! And then...

I would urge people to read Hazel Blear's 2004 pamphlet; 'The Politics of Decency'.

The mountains have travailed and brought forth a ridiculous mouse. The slip in Blears' name is icing.

It's a good speech but that's the only concrete suggestion in there. And you'll notice that there's fuck-all about what to do about "the economic rupture" in there. I therefore conclude that the run-time implementation of this is going to be more fingerwagging about dog dirt and ball games, more youth-hate, and more refugee abuse. Basically, it's the lefty version of John Redwood's shtick about needing to wave the flag as a substitute for the economic security of pre-globalisation (such as it was).

Why exactly should the government be spending hundreds of billions of dollars propping up housing prices.

To avoid a wave of defaults on underwater non-recourse residential mortgages?

To avoid a wave of defaults on underwater non-recourse residential mortgages?

But if you're a born again Hoover/Mellonite, that would be a good thing. What would purge the rottenness from the system more effectively than doing away with such indicators of high living as mass home ownership? Admittedly it would guarantee a depression, but values must be adjusted.

The sword of the Lord and of Gideon (and his transatlantic cothinkers)!

re: 146

Yeah, there's bits in it I find a tad worrying, tbh,* and some of my concerns echo your final paragraph, but I do like the attempt to revive a bit of old-school Labour oratory, which hasn't entirely died out north of the Border, but seems largely a dead duck south of it.

* I usually find the various repeated attempts to revive some sort of civic/secular non-racist egalitarian aspirational English nationalism** both sort of understandable but dreadfully inclined to slip into Dacre-ism/EDL-lite.

** William Blake, Jerusalem, William Morris, rah rah rah, etc. Slow-mo pan over rolling hills and Cornish tin mining hamlets, and Lancashire mills, accompanied by the Grimethorpe Colliery Brass Band, etc.

149.2 We have to uderstand that this sort of shit is now informing ministerial statements:

It's certainly true that apprentices are not the same as they were even a few years ago, never mind in the Victorian era which many people still see as the golden age of apprenticeship.Not policy yet, but this is apparently how they understand on the job training.

If memory serves me right, the conditions in which apprentices worked for much of the nineteenth century were determined by the Health and Morals of Apprentices Act of 1802. And the young learners who are with us this morning might like to reflect on some of the more humanitarian changes that this put in place.

For example, it required apprentices to be given an hour's religious instruction every Sunday and to attend church at least once a month. In my view, that's a rule whose time might well come again.

- John Hayes, Minister of State for Further Education, Skills and Lifelong Learning

148

... What would purge the rottenness from the system more effectively than doing away with such indicators of high living as mass home ownership? ...

How exactly does propping up housing prices promote mass home ownership?

147

To avoid a wave of defaults on underwater non-recourse residential mortgages?

In other words it's still all about bailing out the banks?

87: No better example of greater fool theory. Personally, I'm investing in canned goods and ammo.

Which are even more unresalable than gold in a normal market. Seriously, what?

90: McMegan channels George Bailey as to why a cramdown is a bad thing

I think she's channeling Potter, not Bailey. Also, I feel dumber now that I've read that. Anyways, she isn't talking about a cramdown - a cramdown would involve reducing the principle on the underwater loans and reissuing them. She's talking about a wholesale debt jubilee, which would be fairly excitingly disasterous.

Though I admit, going after a debt jubilee is a great way of avoid talking about a cramdown and cleanup of the existing trashy mortgages.

Sigh.

max

['It always turns out, of course, that we should do nothing. Because nothing can be done.']

I think a very simple summary of the nest of different problems might be useful here:

1. "People might be able to keep their homes because the note can't be produced".

Lots of tax protestor type thinking here. A mortgage note isn't a magic spell. Even if you were able to avoid foreclosure you'd still owe the money. Mortgage borrowers might end up being able to negotiate modifications to the loans from more of a position of strength, is probably the most realistic outcome.

2. "The mortgage bonds which have collapsed will have to be bought back at par!"

Also a bit of tax protestor thinking here, combined with some serious trying-it-on by investors who have unrelated reasons to be suing everyone. The trouble is that for every mortgage you want to put back to the sponsor, you have to litigate to prove both that there has been a failure to establish title and that it's the sponsor's liability to put right. As a way of getting rich, this looks like mining for opals using a plastic spoon.

3: "The entire structure of MERS is illegal".

No real view on this one but so what if it is? If it turns out that the US system of land title has collapsed (maybe it has), then it will have to be re-established. And the basis on which it is established is unlikely to be an egalitarian redistribution or a new series of Land Rushes - it's going to look just like it does now.

4: "Some banks did due diligence on mortgage underwriting and didn't share the results with investors".

Note that this is pretty much completely unrelated to all the rest. Might be a litigable case here - looks a bit like dot com litigation to me though, which showed very few victories despite what looked like a promising case.

5: "The extent to which this is going to be a time and effort sink will stop the mortgage lending market in its tracks, with presumed bad consequences for property prices".

Could happen I suppose.

125

Alas, many great thinkers are obscure to the lay reader, and I hope I can be forgiven if I've gotten James wrong on this. If only there were some way to resolve this conundrum ...

Actually there is. Just add the assumption that Shearer is not an idiot.

I should probably note, btw, that I have a different threshold of what I consider to be "trivial", and given that there are about two dozen big banks involved in this game, if they have to spend two or three billion a year each on clearing up the mess for the next couple of years, that would add up to an amount of money that some people might call "a lot".

Why exactly should the government be spending hundreds of billions of dollars propping up housing prices.

Tell me that you think it would have been wise in 2010 to eliminate the home mortgage interest deduction, and I'll answer your question.

Tell me that you think it would have been unwise to do so, and I'll ask you why exactly should the government be spending hundreds of billions of dollars propping up housing prices.

Actually there is. Just add the assumption that Shearer is not an idiot.

I did that in 4 and got 11, so I'm a little dubious on this strategy.

As a way of getting rich, this looks like mining for opals using a plastic spoon.

Or maybe more like mining for kidney stones with a plastic spoon.

154

For more on point 4 see Felix Salmon here .

154.1: I wasn't thinking of the tax protestors, I was thinking of the "gold fringe on the flag" crowd. Anyway, the farmers who went under in the 80s had some of the same kinds of reasoning about how a minor procedural error* was going to save the farm for them.

*much, much more minor than not having the note.

Lots of tax protestor type thinking here. A mortgage note isn't a magic spell. Even if you were able to avoid foreclosure you'd still owe the money.

But owe it to whom?

157

Tell me that you think it would have been wise in 2010 to eliminate the home mortgage interest deduction, and I'll answer your question.

Tell me that you think it would have been unwise to do so, and I'll ask you why exactly should the government be spending hundreds of billions of dollars propping up housing prices.

So one government stupidity justifies any additional government stupidity?

Regarding mortgage interest, in theory I consider this a legitimate deduction from income. (More precisely that portion of mortgage interest that exceeds the inflation rate but the failure of the tax system to account for inflation is a whole nother can of worms.) If interest received is income, interest paid should be deductible. The loophole is the failure to include the imputed rental value of the house in income. But as a practical matter perhaps just eliminating the mortgage deduction is the way to go (although this favors cash buyers). However also as a practical matter eliminating a long standing popular (albeit misguided) flaw in the tax code was probably not the best use of scarce political capital in 2010. Not that I like what Obama did use his political capital for.

But this is no justification for adding a new extremely expensive and damaging subsidy.

So one government stupidity justifies any additional government stupidity?

No, James. The mortgage interest deduction costs the US huge amounts of money. This isn't "additional" stupidity, this is the exact sort of public policy choice you described with your question in 145. I was trying to get you to answer your own question, to see what your policy preferences actually are.

This might be responsive, but I'm not sure:

However also as a practical matter eliminating a long standing popular (albeit misguided) flaw in the tax code was probably not the best use of scarce political capital in 2010.

Just to make sure, let me ask again: Purely as a matter of public policy, and leaving aside the actual possibility of doing so, should the mortgage interest deduction have been eliminated in 2010? I take your answer to be "yes, it should have been eliminated." Have I got that right?

If interest received is income, interest paid should be deductible.

This makes no sense at all. Money I earn by mowing other people's lawns is income, therefore money I pay other people to cut my lawn should be deductible?

(I know, analogy ban)

154.2: This doesn't look as obviously not-a-serious-issue to me as all that.

The trouble is that for every mortgage you want to put back to the sponsor, you have to litigate to prove both that there has been a failure to establish title and that it's the sponsor's liability to put right.

The sponsor's liability to put it right can be litigated in bulk -- if that's the terms on which the mortgage bonds were sold, the same terms should apply to all the underlying mortgages. If I were a plaintiff, I'd try to bifurcate the action, establish liability for each mortgage with improperly established title, and then do thousands of little hearings on each mortgage. It'd be a full employment for lawyers proposition, but if a significant percentage of the mortages weren't properly transferred, it'd be worth doing.

and then do thousands of little hearings on each mortgage.

It is a minor worry in the greater picture of the mortgage crisis, but I do worry about the small mortgages and what happens if nobody wants to pay to litigate them. My guess is that these small mortgages are more likely than usual to be recorded poorly. Anyway, I'd hate to have a large number of $10k to $50k houses where the title is in limbo. That could damage some of the neighborhoods near me in a way that the actual foreclosures haven't.

Well, in the context of what I'm talking about, the people who bought mortgage-backed securities would have an incentive to litigate all of them, but that doesn't solve the problem you're talking about.

The problem you're talking about could turn out to be significant -- houses that no one can establish title without spending more than the house is worth on litigation -- and I'm not sure how that gets fixed.

From what I've seen around here, when the sale of tax liens produced a similar problem, is that things drag out until the house isn't worth anything at all (which, to be fair, may have been what would have happened regardless). They city had sold a bunch of liens to somebody, but the houses were quickly worth less than the lien because that's what happens to a house that isn't maintained in a depopulating city. After several years, whoever bought the liens gave up and sold them back to the city for cheap and the city is hunting bits of money to push them over.

For a while, my father worked for the NYC department of Housing Preservation and Development supervising rehabs of buildings that had been forfeited to the city on tax liens, but of course that was multi-unit buildings in NYC, not cheap houses someplace less dense. I dunno, is there an oversupply of housing? Maybe razing some houses is the right thing to do? Not in cases where there's a person living there, but an uninhabited house with no clear owner?

I wasn't clear enough. I'm worried about the delay before razing, not the razing. The city was (is?) willing to condemn a house and wait for the owner to destroy it even when there isn't an owner or the owner has no resources or the owner doesn't care.

167 gets it right. Whatever the problems are with 154.2 (which seems to me the biggest issue) it's not that it would be impossible to litigate.

154.4 is the kind of thing plaintiffs lawyers have been trying to show since Day 1 of the crisis, with very little success so far.

Actually, I don't think 154.2 would be all that hard: the actual facts of what documents are, or are not in the possession of whom, and which loans do, and do not, conform to certain specific requirements of the documents, are objective matters. Rogs and requests for admissions ought to be able to get the facts resolved in fairly short order. (Rogs, RFAs, and motions to compel). Liability is simply a matter of the documents.

And once someone wins one, or even just gets partial summary judgment on a claim, demands are going to get taken seriously enough that settlements get possible and big.

Maybe the biggest disincentive, though, is the same one that's held up a bunch of foreclosures: no one, not even investors, wants to admit that the emperor's got no clothes. Everyone, including investors, is carrying crap on their books, and recognizing true value hurts everyone.

not even investors, wants to admit that the emperor's got no clothes.

The emperor has a beautiful ass, that's why.

Actually the issue with respect to #2, which I didn't set out very clearly, presumably because I'm not an American lawyer, is that despite what Felix and Mike say in their potted summaries, the language in the bonds just doesn't unambiguously say "if there was a problem with the documentation, you can put the mortgage back at par". If the liability was as clear-cut as that, I doubt that there would ever have been a problem like this allowed to develop in the first place.

What the docs actually do say that the sponsoring bank has to "take remedial actions, including if applicable the repurchase" of the loan. Turning "remedial actions" into an obligation to purchase a near-worthless mortgage at par is the "digging for opals" part, and this does have to be done on a loan by loan basis, because it has to be decided in every case what the "remedial action" appropriate to the case is. Nearly everyone seems to already be giving up on putbacks, - unless someone knows different , no major vulture fund has taken this one on. The action is in different kinds of litigation, with putback lawsuits largely used as a harassment technique.

176 is exactly what I was looking for. As you note, it seemed highly improbable that this situation arose if there were contracts that unambiguously said that problems with documentation=repurchase at par, but no one was spelling out what the contracts do, in fact say.

"arose" s/b "could have conceivably arisen"

and this does have to be done on a loan by loan basis, because it has to be decided in every case what the "remedial action" appropriate to the case is.

Huh. I'd think you could still do it in bulk -- litigate over some large group of mortgages covered by the same documents and get a ruling on what the facts would have to be to justify compelling a repurchase, and then case by case hearings on whether individual mortgages met that standard.

After researching the specifics, the facts might not be bad enough to make it worth doing, but it doesn't sound procedurally unworkable to me.

One thought: Title insurance and all that was already a scam before all of this happened. There were already robo-signers, but nobody really cared because it sped up the process and most people were getting second mortgages and refinancing rather than getting foreclosed on. Back in 2006 my accounting prof assigned us an article about how messed up all of that stuff is -- basically due to a lot of entrenched interests that had mutated state laws around titles and deeds so that a lot of easy money could be made by banks and real estate firms. It was pretty shocking.

Another thought: Just in the past few weeks, just on my 2 mile walking route to work, I've seen three houses demolished. They were all pretty far gone -- legitimately derelict, and not just tied up in back taxes or whatever -- but it was still kinda shocking. I live in a poor neighborhood, yeah, but one with a pretty high degree of home ownership, a lot of activists and an active, engaged neighborhood association that often gets things done at City Hall.

Final thought: An acquaintance of mine runs a local Neighborhood Housing Service non-profit, that rehabs old houses, as well as providing a lot of other housing-related services. He's been doing it for some time, literally buying 10 houses in a week on some occasions, and I ran into him downtown a couple of months ago, where he was cooling his heels because the bank had screwed up one small signature line on one document, and it was holding up the whole transaction. I realize that buying a house has to include some degree of legal complexity, but surely, after all of this mess, there's some traction to be found for a wholesale reform of real estate transaction law? I know, Commerce Clause, yadda yadda yadda, but all of this stuff you read about how screwed up things are, surely a proposal for real reform is not a complete non-starter?

Right, but it sounds like the problem isn't so much figuring out how to procedurally aggregate the litigation, for which there's almost always a solution, but figuring out the underlying liability -- and it sounds like there's not much underlying liability, assuming that appropriate "remedial action" means (as it likely does) something like "taking reasonable steps to help fix the paperwork problem."

Anyhow, thanks. The way the summaries of the problem were presented always seemed to miss the key element of what the contracts actually say, which is the key to the entire situation.

180.last: Property law is one of the weirdest, most archaic areas of the law, with all kinds of stuff left over from feudal England. I just got done reading about a bunch of doctrines that still exist that were originally invented to prevent medieval tax evasion.

About razing abandoned homes: One real problem is that it costs money, more than cities have these days. This is an excellent, if slightly out of date, piece on foreclosures, abandonment, razing, and how it all affects neighborhoods.

This shit ain't just recent, either. We bought our place in 2004, went to refi in 2009 and found out that the previous owners had a mortgage that was transferred to some other entity and the transfer document was never signed. Probably that was carelessness, not fraud, since in fraud they get some janitor to sign everything, but still a mess from >6 years ago. Supposedly it was straightened out at no cost to me (hurray title insurance! I remember thinking that was a huge scam every time I paid it) but it's not quite clear to me how- they perfected the title by having someone file some affadavit attesting to something or other.

I also remember having to pay some fee for MERS at the first closing and wondered what that was all about...

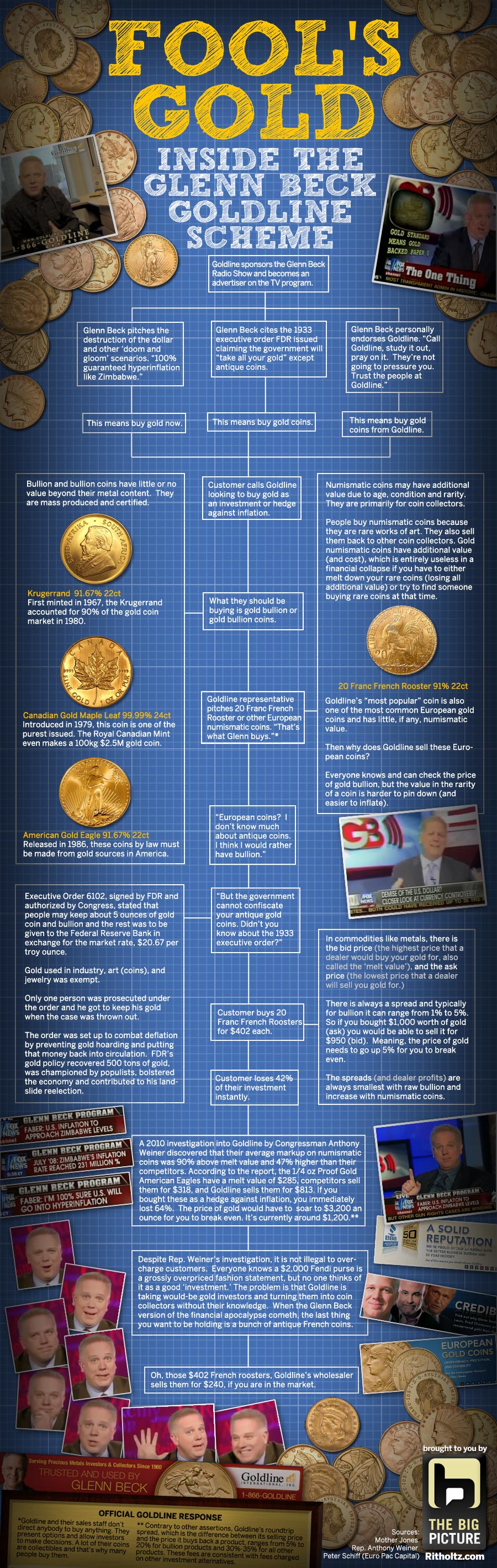

I'm not familiar with how the gold stuff Beck pushes works- do they send you actual physical gold? If so, how do you verify the amount and purity they claim? If not, and I always assumed that you just get a certificate or electronic record saying you own some gold somewhere rather then getting actual slips/strips/bars, how is it any different in terms of apocalyptic reliability from any other security?

I'm waiting for the scam to blow up on those companies (beyond the scam of the 30-50% fees they charge) where it turns out they don't actually have any gold, they've just been taking people's money, or maybe sending them some nice pyrite.

Maybe they send you Gold Bond powder, to feel the true tingle of freedom.

184: I'm not familiar with how the gold stuff Beck pushes works- do they send you actual physical gold? If so, how do you verify the amount and purity they claim?

They're selling actual physical coins, as far as I know, having seen just a few ads. They're not advertising for investing in various types of gold funds, although there is a lot of that going on elsewhere. IIRC, what Beck is pimping for involves vastly overpriced coins (versus the purchasing the equivalent amount of gold at the spot price), so they're essentially ripping people off at price that's something like four times the spot price.

As for the amount and purity, well, you don't verify it, really, except with very good scales and some chemistry. I expect almost no one does that.

max

['The man certainly knows how to grift.']

This isn't going to be sorted out by letting the banks just foreclose everybody.

max

['Well, if it is, it's going to be really ugly.']

Forgot to close the link. Sorry.

max

['Gah.']

I'm not familiar with how the gold stuff Beck pushes works- do they send you actual physical gold?

This is the other end of the scam, but there are two store fronts within walking distance of my house that advertise they buy gold jewelry. This makes me wonder about the future of our mini commercial district.

186: I think it is legit at this point to simply refer to Beck as a gold salesman.

184: they try to sell you antique gold coins for an enormous markup.

I almost got a gold crown, but my dentist didn't like Beck (except for Beck the musician) and I got a boring crown that looks pretty much like the tooth before the crown unless you take an x-ray. It looks very different on x-ray.

I got a gold crown, but nobody died and made me king.

{kind=link}